4. Types of Health

Insurance (HMO, PPO, POS)

·

Indemnity plans vs. managed care

·

HMOs, PPOs, POS Plans

·

Group health insurance

·

Individual health insurance

·

Vision care insurance

·

Dental insurance

·

Medicare

·

Medicaid

·

Medigap insurance

·

Health insurance plans can be broadly

divided into two large categories:

(1) Indemnity plans(also

referred to as “ reimbursement “ plans), and

(2) Managed care

plans.

·

Indemnity plans

·

An indemnity plan reimburses you for

your medical expenses regardless of who provides the service ,although in some

cases your reimbursement amount may be limited .The coverage offered by most

traditional insures is in the form of an indemnity plan.

·

Under this type of plan, the insurer pays

a specified amount per day for a specified maximum number of days. Although you

reimbursement amount does not depend on the actual cost of you care, your

reimbursement will never exceed your expenses.

How is benefit amount calculated with an indemnity plan?

Different plans use different method for determining

how much you will receive for your medical expenses .Following and descriptions

of the most common methods.

Reimbursement-actual

charges

Under this type of plan, the insures will reimburse

you for the actual cost of specified procedures or services, regardless of how

much that cost might be.

Reimbursement-Percentage

of actual charges

Under this type of plan, the insurer pays a

percentage of the actual charges for covered procedures and services,

regardless of how much those procedures and services cost. A common reimbursement

percentage is 80percent.This has the same effect as a 20 percent co-payment.

· Managed care plans

There are three basic types of managed care health insurance

plans:

1. Health

maintenance Organizations(HMOs),

2. Preferred

Provider Organizations(PPOs),and

3. Point

of Service (POS) plans.

a. Health maintenance Organizations

(HMOs):

·

A health maintenance organization (HMO)

is a type of managed healthcare system.

·

HMOs share the goal of reducing

healthcare costs by focusing on preventive care and implementing utilization

management controls

·

HMOs do not merely provide financing for

medical care; they actual delivers the treatment as well.

·

Doctors, hospitals, and insures all

participate in the business arrangement known as HMO.

·

HMOs provide medical treatment on a

prepaid basis, which means that HMO members pay a fixed monthly fee, regardless

of how much medical care is needed in a given month.

·

Most HMOs provide a wide variety of

medical services, from office visits to hospitalization and surgery. With a few

exceptions, HMO members must receive their medical treatment from physicians

and facilities within the HMO network. The size of this network varies

depending on the individual HMO.

·

When you join an HMO, you choose a

primary care physician (PCP) who is your first contact for all medical care needs.

The primary care physician provides your general medical care and must be

consulted before you can see a specialist.

Advantages of HMOs

· Low out-of-pocket costs

· HMO members pay a fixed monthly fee, regardless of how much medical care is needed in a given month, Instead of deductibles, HMOs often have nominal co-payments.

· Focus on wellness and preventive care.

· By reducing out-of-pocket costs and paper work ,HMOs encourage members to seek medical treatment early, before health problems become severe

· Many HMOs offer health education classes and discounted health club memberships.

· Typically no lifetime maximum payout

· HMOs generally do not place a limit on your lifetime benefits. The HMO will continue to cover your treatment as long as you are a member.

Disadvantages of HMOs

·

Tight controls can make it more

difficult to get specialized care

·

As an HMO member, you must choose a

primary care physician (PCP).Your PCP provides your general medical care and

must be consulted before you seek care from another physician or specialist.

·

This screening process helps to reduce

costs both for the HMO and for HMO members, but it can also lead to

complications if your PCP doesn’t provide the referral you need.

·

Care from non-HMO providers generally

not covered

·

Except for emergencies occurring outside

the HMO’s treatment area, HMO members are required to obtain all treatment from

HMO physicians.

b. Preferred Provider Organizations

(PPOs):

·

Like an HMO, a preferred provider Organization

(PPO) is a managed healthcare system, where a group of doctors and/or hospitals

that provides medical service only to a specific group or association.

·

The PPO may be sponsored by a particular

insurance company, by one or more employers, or by some other type of

organization.

·

PPO physicians provide medical services

to the policyholders or members of the sponsors (s) at a discounted and may set

up utilization control programs to help reduce the cost of medical care.

·

PPO members pay for services as they are

rendered. The PPO sponsor (employer or insurance company) generally reimburses

the member for the cost of the treatment, less any co-payment percentage.

·

The price for each type of service is

negotiated in advance by the healthcare providers and the PPO.

Advantages of PPOs

·

Free choice of healthcare provider – PPO

members are not required to seek care from PPO physicians. However, there is

generally strong financial incentive to do so.

For example, members may receive 90% reimbursement for care obtained

from network physicians but only 60% for non-network treatment .In order to

avoid paying an additional 30% out of their own pockets, most PPO members choose

to receive their healthcare within PPO network.

·

Out- of-pocket costs generally limited

–Healthcare costs paid out of your own pocket (e.g. Deductibles and

co-payments) are limited.

·

Typically, out-of-pocket costs for

network care are limited to $1200 for individuals and $2,100 for families.

·

Out-of-pocket costs for non-network

treatment are typically capped at $2000 for individuals and $3500 for families

Disadvantages of PPOs

·

Less coverage for treatment provided by

non-PPO physicians

·

More paperwork and expenses than HMOs

As a PPO member, you may have to

fill out paperwork in order to be reimbursed for medical treatment.

Additionally, most PPOs have larger

co-payment amounts than HMOs, and you may be required to meet a deductible.

c. Point of Service (POS)

Plan:

· A point of service (POS) plan is a type

of managed healthcare system that combines characteristics of the HMO and the

PPO.

·

Like an HMO, you pay no deductible and

usually only a minimal co-payment when you use a healthcare provider within

your network.

·

Must choose a primary care physician who

is responsible for all referrals within the POS network.

·

If you choose to go outside the network

for healthcare, POS coverage functions more like a PPO. In such case,

Deductible may apply around $300 for an individual or $600 for a family, and

your co-payment will be a substantial percentage of the physician’s charges (usually

30 -40).

Advantages of POS

Plan:

·

Maximum

freedom – POS coverage allows you to maximize your freedom of choice.

Like a PPO, You can mix the types of care you receive, For example, your child

could continue into see his pediatrician who is not in the network, while you

receive the rest of your healthcare from network providers. This freedom of

choice encourages you to use network providers but does not require it, as with

HMO coverage.

·

Minimal

co-payment – You pay only a nominal amount of co-payment for network

care .Usually your co-payment is around $10 per treatment or office visit.

Unlike HMO coverage, however, you always retain the right to seek care outside

the network at a lower level of coverage.

·

No

deductible – When you choose to use network providers, there

is generally no deductible.

·

No

“gatekeeper “for non –network care –if you choose to go outside

the POS network for treatment, you are free to see any doctor or specialist you

choose without first consulting your primary care physician (PCP). Of course, you

will pay substantially more out-of -pocket charges for non-network care.

·

Out-of-pocket

costs limited –Healthcare costs paid out of your own

pocket are typically limited.

Disadvantages of POS Plan:

·

Substantial

co-payment for non-network care – As in PPO there is

generally strong financial incentive to use POS network physicians.

For

ex.

Your co-payment may be only $10 for care obtained from network physicians, but

you could be responsible for up to 40% of the cost of treatment provided by

non-network doctors. Thus, if your longtime family doctor is outside of the POS

network, you may choose to continue seeing her, but it will cost you more.

·

Deductible

for non-network care – In most cases, you must reach a

specified deductible before coverage begins on out-of-network care. On average,

individual deductibles are around $300 per year, and the average annual family

deductible is about $600 .This deductible amount is in addition to the

co-payment for out-of-network care.

Tight

controls to get specialized care –As in an HMO, you

must choose a primary care physician (PCP).Your PCP provides your general

medical care must be consulted before you seek care from another doctor or

specialist within the network.

5. Provider vs. Payer, and NPI

Provider:

· A health care provider is an individual, group, or organization that provides medical or other health services or supplies. This includes physicians and other Practioners, Physician/ Practioner groups, Institutions such as hospitals, laboratories, and nursing homes, organizations such as hospitals, laboratories, and nursing homes, organizations such as health maintenance organizations, and suppliers such as pharmacies and medical supply companies.

· This does not include health industry workers, such as admissions and billing personnel, housekeeping staff, and orderlies, who support the provision of health care but do not provide health care services.

· Health care provider is “a person or organization---that provides health care or medical care services for a fee. You can submit a health care claim (CMS-1500, UB-04, ADA, and NCPDP) to a payer (group purchaser) or an invoice, and get reimbursed for that service.

Payer:

·

Health care generally refers to entities other than the

patient that finance or reimburse the cost of health services. In most cases,

this term refers to insurance carriers, other third-party payers, or health

plan sponsors (employers or unions)

·

Payer organizations focus on managing the gap between

funding and medical costs, often in the context of a changing regulatory

environment at the state and the federal level.

· The NPI is a unique identification number for health care providers that will be used by all health plans. Health care providers and all health plans and health care clearinghouses will use the NPIs in the administrative and financial transactions specified by HIPAA.

· The NPI was proposed as an 8-position alphanumeric identifier. However, many preferred a 1 position numeric identifier with a check digit in the last position to help detect keying errors.

How would NPIs be issued?

NPIs would be issued by the National Provider System(NPS).The NPS organization members would carry out a number of functions, which include entering identifying information about a health care provider into the system, performing data validation(for example, confirming the state license number),notifying a healthcare provider of its NPI.

NPIs would be issued by the National Provider System(NPS).The NPS organization members would carry out a number of functions, which include entering identifying information about a health care provider into the system, performing data validation(for example, confirming the state license number),notifying a healthcare provider of its NPI.

What are the uses of the NPI?

· Health care providers to identify themselves in health care transactions identified in HIPAA or on related correspondence.

· Health care providers to identify other health care providers in health care transactions or on related correspondence.

· Health care providers on prescriptions.

· Health plans to coordinate benefits with other health plans.

· Health care clearinghouses in their internal files to create and process standard transactions and to communicate with healthcare providers and health plans;

· Electronic patient record systems to identify treating health care providers in patient medical records.

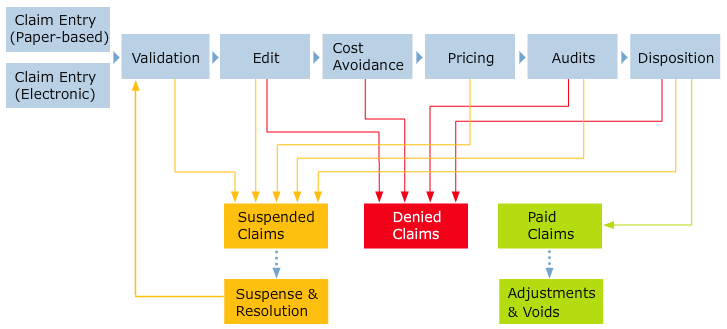

1. Claims process flow:

The graphic below shows the process flow for the claim life cycle.

The following table describes the phases of the claim life cycle depicted in the graphic above:

Phase

|

Description

|

Claim Entry

|

In the claim entry phase, a claim enters the process as either a:

If claims are submitted as paper documents, the EDMS staff scans them so they are available in MITS. The EDMS staff also enters the required data, verifies the data, and corrects any data identified as incorrect during the scan process. Claims are either Encounter Claims or Fee-for-Service Claims. The claim then proceeds to the Validation phase.

|

Validation

|

MITS automatically performs validation using provider contracts, recipient benefit plans, and reference code set information to validate a claim. MITS validates recipient eligibility, provider eligibility, procedure codes, diagnosis codes, provider contract eligibility, reference data, and BPA rules. If Prior Authorization is required, MITS validates PA rules as well. If it passes all validations, it proceeds to the Edit phase. If the claim does not pass the validations, it proceeds to the Suspended Claims phase.

|

Edit

|

During this phase, MITS automatically performs edits on the claim against the business rules. MITS may deny or suspend a claim at this time. If the claim is suspended, it proceeds to the Suspended Claims phase. If the claim passes all edits, the claim proceeds to the Cost Avoidance phase.

|

Cost Avoidance

|

In this phase, MITS automatically determines if a claim will not be paid due to factors such as other payers. If there is a third-party responsible for the claim, MITS denies the claim. MITS has Third Party Liability (TPL) functionality to ensure that Medicaid is the payer of last resort. The TPL function works with a combination of cost avoidance and cost recovery. If there isn’t a third party liable, the claim proceeds to the Pricing phase.

|

Pricing

|

After MITS validates a claim and the claim passes all edits, MITS calculates the amount to pay by identifying the establishing pricing indicator and rate type. In this phase, MITS also determines if prior authorization rates exist. If manual pricing is required, MITS suspends the claim and the claim proceeds to the Suspended Claims phase. If manual pricing is not needed, the claim proceeds to the Audits phase.

|

Audits

|

In the audit phase, MITS automatically verifies the claim service data against other claims in history OR other details for the same claim for the same recipient. MITS verifies the claim conforms to state policy and checks for:

If the claim has any issues based on these checks, MITS can either suspend the claim or deny it. If the claim is suspended, it proceeds to the Suspended Claims phase. If no issues exist, the claim proceeds to the Disposition phase.

|

Disposition

|

In this phase, each claim is given a status of paid, denied or suspended based on the disposition of edits and audits. A claim can pay or deny without user interaction in MITS. If a claim suspends, it proceeds to the Suspended Claims phase, where the data correction staff reviews the claim and must determine a course of action such as pay or deny. The claim then reprocesses through the claim life cycle after data corrections are complete.

|

Suspended Claims

|

If a claim is suspended, MITS reassigns the claim for review. Data correction staff makes corrections to move toward resolution. After proceeding through the Suspense and Resolution phase, the claim then recycles through the phases of the claim life cycle.

|

Suspense and Resolution

|

This phase is part of the Suspended Claims phase. If the status is suspended, the data correction staff performs the following actions to move toward resolution:

|

Denied Claims

|

If a claim is denied, MITS sets the final status to denied and moves the claim to denied history.

|

Paid Claims

|

If a claim is paid, MITS has completely processed it. It has passed through all phases with no resulting issues so that payment is made to the provider. The final status is paid. Encounter Claims also have a paid status, but the Managed Care Plan/Organization makes payment to the Provider.

|

Adjustments and Voids

|

Claims in a paid status can be adjusted and voided. These are completed in MITS for paper-based requests that are scanned.

|

Manual Claims Processing vs Automated Claims Processing

2. Claims submission:

Electronic Medical Claims submission (EMC):

· EMC is an electronic claims processing system that enables a provider to submit his/her claims to the carrier more efficiently than the paper claims. Provider can submit claims by modem, by magnetic computer tape or by floppy diskette.

· Paper submission on different forms(such as CMS1500,CMS1450 or UB92,ADA992000)

· How to Submit Claims: Claims may be electronically submitted to a Medicare Administrative Contractor (MAC) from a provider using a computer with software that meets electronic filing requirements as established by the HIPAA claim standard and by meeting CMS requirements contained in the provider enrollment & certification category area of this web site and the EDI Enrollment page in this section of the web site. Providers that bill institutional claims are also permitted to submit claims electronically via direct data entry (DDE) screens.

How Electronic Claims Submission Works: The claim is electronically transmitted from the provider's computer to the MAC. MACs The initial edits are to determine if the claims meet the basic requirements of the HIPAA standard. If errors are detected at this level, the entire batch of claims would be rejected for correction and resubmission. Claims that pass these initial edits, commonly known as front-end edits, are then edited against implementation guide requirements in those HIPAA claim standards. If errors are detected at this level, only the individual claims that included those errors would be rejected for correction and resubmission. Once the first two levels of edits are passed, each claim is edited for compliance with Medicare coverage and payment policy requirements. Edits at this level could result in rejection of individual claims for correction, or denial of individual claims. In each case, the submitter is sent a response that indicates the error to be corrected or the reason for the denial. After successful transmission, an acknowledgement report is generated and is either transmitted back to the submitter of each claim, or placed in an electronic mailbox for downloading by that submitter.

Claims Adjudication Process - How Health Insurance Companies Process Claims

How Electronic Claims Submission Works: The claim is electronically transmitted from the provider's computer to the MAC. MACs The initial edits are to determine if the claims meet the basic requirements of the HIPAA standard. If errors are detected at this level, the entire batch of claims would be rejected for correction and resubmission. Claims that pass these initial edits, commonly known as front-end edits, are then edited against implementation guide requirements in those HIPAA claim standards. If errors are detected at this level, only the individual claims that included those errors would be rejected for correction and resubmission. Once the first two levels of edits are passed, each claim is edited for compliance with Medicare coverage and payment policy requirements. Edits at this level could result in rejection of individual claims for correction, or denial of individual claims. In each case, the submitter is sent a response that indicates the error to be corrected or the reason for the denial. After successful transmission, an acknowledgement report is generated and is either transmitted back to the submitter of each claim, or placed in an electronic mailbox for downloading by that submitter.

Payments and Denials:

Payments: Amount Paid to the physicians against the services rendered by them to the patient.

(THE SERVICES THAT ARE PROVIDED TO THE PATIENTS ARE SENT OUT TO THE INSURANCE COMPANIES IN THE FORM OF CLAIMS.THESE CLIAMS GET PAID BY THE INSURANCE COMPANIES.THE PAYMENTS ARE RECEIVED AT THE PROVIDER’S MAILING ADDRESSES AND /OR AT THE BILLING COMPANIES ADDRESSES.IN CASES WHEN THEY ARE RECEIVED AT THE PROVIDERS’ADDRESSES THEN THEY ARE IN TURN FORWARDED TO THE BILLING COMPANY TO THE APAYMENT IN THEIR SYSTEM.SUCH PAYMENTS COME IN THE FORM OF BATCHES AND MAY HAVE BANK’S DEPOSIT SLIP OR PAYMENT LISTING WITH THEM.PAYMENTS THAT ARE RECEIVED DIRECTLY AT THE BILLING COMPANIES ADDRESS DO NOT HAVE THE BANK’S DEPOSIT SLIP.)

SOMETIMES IN THE CASE OF NON-PARTICIPATING PROVIDER’S .PAYMENTS ARE RECEIVED BY THE INSURED PARTIES ADDRESS AND THEY FORWARD THE PAYMENT TO THE PHYSCIANS ADDRESS

Denials:

Claim that do not get paid, come back as Denials from the insurance carriers. This can be due to posting errors, incorrect procedure /diagnosis code, lack of information (medical records) while filing the claims, or missing/incomplete patient details.

Denials are broken down into two categories: In-House and patient Responsibility.

· In-House denials are the ones that require some type of correction from our part and can be resubmitted. We do not bill patient.

· Patient Responsibilities are those denials that we can’t do anything to get the claim paid by the insurance company. All we can do is, transfer the charge to the patient with the correct message code.

3. Claims Adjudication Processing

· Claims adjudication can be a quick process when a clean claim is received. "Clean" in this case means that all the information on the claim is correct and within the bounds of the patient's healthcare policy.

· When medical review is involved there's a delay waiting on staff and documentation requested to be received and reviewed.

· The claims adjudication process has improved recently because of the great advances in software and the edits created. This process collects a large amount of information, verifies it, and issues payment. This is a great improvement over the "hands and eyes" on every paper claim form in the past!

Claims Adjudication Process - How Health Insurance Companies Process Claims

What happens after medical billers send a claim? This describes how insurance companies determine payment to healthcare providers: the claims adjudication process.

Most healthcare services are paid by third party payers in the United States. This includes Medicare, Medicaid other government services and private insurance companies.

Medicare and Medicaid (CMS) have very specific rules regarding the submission of claims for payment of services provided. The rules and benefits are published for all patients types. The software Medicare and Medicaid use is extremely precise when verifying submitted claims.

Private insurance companies have a variety of plans with many different rules. These rules mean that each claim has to be examined very closely. Software edits have been developed that performs all of these tasks except the medical review.

Receiving the claim

Because the claim form is received electronically by the insurance company, software begins the review of the information. The claims are placed in a "lineup" and start through the claims adjudication process.

The unique identification number assigned to the patient is the first piece of information that the software verifies. This number allows the software edits to recognize all the information associated with the insurance plan assigned to the patient.

The patient's name must be associated with the ID number. If this doesn't match, then the claim adjudication may end at this step. A rejection letter will be sent to the physician and to the patient with the explanation of denial. This may be sent by mail or electronic means.

The software edits continues to verify date of birth and gender. Each step may trigger a stop and rejection notification if information isn't attached to the ID number.

Date of service and place of service information is verified as allowed by the plan benefits associated with the unique identification number. Date of the claim submission is compared with the edit for days allowed to submit a claim for payment.

Many insurance plans require prior authorization or approval before an office visit or procedure is performed. The insurance company provides a referral number that must be added to the claim. If this number isn't supplied, the claim will be rejected.

The medical information in the form of the procedural codes (CPT) and diagnosis code (ICD-10) are vital information on the claim. The software matches the procedure with the diagnosis code or medical reason for the service provided.

The software then confirms that the procedure is included in the insurance plan. At this point the software can reject the claim or send for medical review.

The claim continues through the software to validate the physician's name and National Provider Identifier (NPI) designation that was submitted. The edits will verify if the physician has a contract with the insurance company or is an out-of-network physician. This will be used in determining the amount to reimburse.

The software reviews the patient's co-pay and any other payments to determine if the patient's portion of payment has been made and subtracted from the billed amount.

When the claim has made it through the software edits without any errors, the claim will be paid at the contractual rate. A check in the mail or electronic payment will be made with the issue of a remittance advice.

The remittance advice explains to the physician with a copy to the patient how the payment was determined.

Medical Review

The software edits send the claim for medical review. The software has been developed to determine the procedural codes and/or the medical diagnosis codes that the insurance company needs to review.

This edit can be used for more expensive procedures and/or to verify the physician's credentials for billed procedures.

As this process takes place the claim is suspended, and is deemed in "development" as new information is obtained to continue with the claims adjudication process.

In the medical review process, the claim is sent electronically to the medical review desk. A nurse will review the information on the claim. The nurse will be able to review the policy and prior claims of the patient to determine the medical necessity and appropriate procedure.

The nurse might request additional information from the physician and/or the patient. A letter sent by electronic means or by mail may request copies of the patient's chart, lab tests, x-rays and other medical information that the nurse needs to determine the medical necessity of the claim.

The claim remains in suspension and in development while the information is received and reviewed.

After the nurse reviews this information he or she can approve or deny payment for the claim. The nurse has the option to involve the doctors on the insurance staff to review all documentation.

The doctors are the final authority in determining to pay or reject the claim based on criteria set by the medical staff and the insurance company. Letters are sent to the physician and the patient with the information of the medical review.

If approved payment is made. If payment is, denied there is an appeal process for the physician and patient.

4. Compliance Check

Compliance:

Compliance is either a state of being in accordance with established guidelines or specifications, or the process of becoming so. Software, for example, may be developed in compliance with specifications created by a standards body, and then deployed by user organizations in compliance with a vendor's licensing agreement. The definition of compliance can also encompass efforts to ensure that organizations are abiding by both industry regulations and government legislation.

No comments:

Post a Comment